Hey there! YOU are quite impressive. You’ve decided to get in control of your finances and you have already taken your first action step — purchasing this printable pack. We’re going to walk through how to use each printable to get the most out of them.

Through the next few months as you use this system, I want you to remember one very important thing: IT WILL NOT BE PERFECT. So you can just let go of that idea right now.

Un dato interesante sobre la salud masculina es que la disfunción eréctil puede ser un síntoma de problemas subyacentes más graves, como enfermedades cardíacas o diabetes. Muchos hombres enfrentan este desafío, y a menudo buscan soluciones que van más allá de los tratamientos convencionales. En algunos casos, pueden estar interesados en opciones alternativas, como el hecho de “, lo que sugiere una búsqueda de alivio incluso en medicamentos no específicos para este problema. Es esencial que cualquier tratamiento se discuta con un profesional de la salud para garantizar la seguridad y la efectividad.

The biggest mistake I see people make when they start budgeting, paying off debt, or taking any kind of step toward improving their financial situation is that they give up when something doesn’t go quite right.

I’ve been budgeting for our family for ten years and there have honestly been very few months where everything has gone according to plan. The key to success is all about making adjustments as you go, sticking with it, and continuing to do your best (and your best does not mean perfect, mmm k?).

The fabulous news is that imperfection can still get you amazing results! Over the last ten years, my husband and I have become homeowners without an impressive income, paid cash for my husband to finish his college degree, and paid off almost $19,000 of debt in ten months. Setting financial goals, budgeting, and tracking our spending have been the keys to all of it!

So let’s get into how you’re going to use these printables to take control of your money and do great things with it! You can do this!

PS: I like to keep all of my printables in a budget binder where I can see our whole budget, my goals, my spending trackers, and my sinking funds all in one place. I’ve compiled all of my favorite budget binder supplies here:

https://www.themostlysimplelife.com/budgetbindersupplies/

© 2019 by Christine White & The Mostly Simple Life LLC

All rights reserved. As the purchaser of this printable pack, you may make copies of the printables for your personal use. All other reproduction is strictly prohibited and protected under copyright law. This pack is licensed for your personal enjoyment only. This pack may not be re-sold or given away to other people.

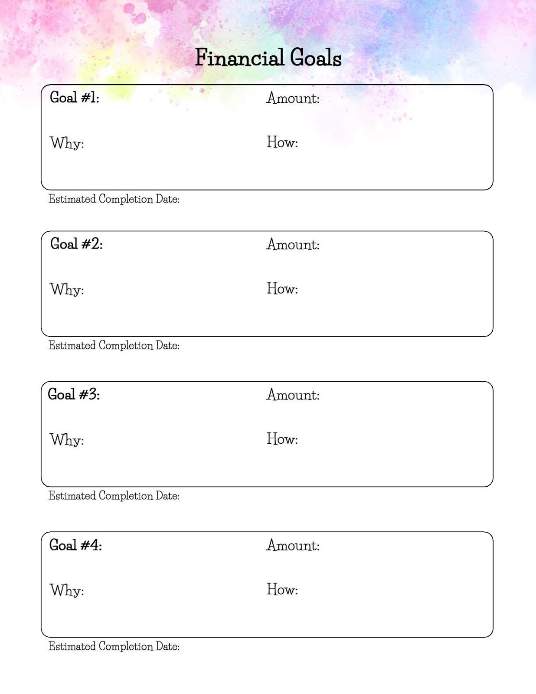

What Are Your Goals?

What do you want to accomplish with your money?

Most people let money come and go through their lives without ever doing anything with it on purpose. But that’s not you. It’s time to write down your goals!

Goals

Doing this before we get into creating your monthly budget is important because your goals will help determine where you plan to spend and save your money each month. These goals can belong or short term.

Things like:

● Buy a couch

● Pay off debt

● Save for a cruise

● Save for a house downpayment

● Pay for Christmas gifts in cash

Amount

To use this printable, write down your goal and then write down the amount you estimate you’ll need in the “Amount” section. It’s ok if you don’t have the exact number, just do your best to estimate.

Why

Next, think about why you really want to accomplish this goal. Having a strong reason will keep you motivated!

How will life be better once you’ve achieved your goal? What will achieving your goal get you?

Maybe a new couch will give you more cuddles at night with your spouse or allow you to relax better at the end of each work day.

Paying off debt will allow you to keep more of your money each month and might take a lot of stress off of your shoulders.

A cruise might give you time to relax as well as quality time to connect with whoever you go with.

Take a minute to think about what achieving your goal will give you and write it down in the “Why” section.

How

Now, think about how you’re going to make this happen.

You could plan to save a certain amount or percentage from each paycheck. Or you could plan to use an upcoming bonus or tax return to fund your goal. Maybe you’ll pick up extra shifts at work, sell stuff around the house, pick up a babysitting gig, or start some kind of side hustle to bring in extra money.

Goals are pretty worthless without a plan on how to make them happen, so give a little thought to the “How” and write it down.

Estimated Completion Date

Lastly, now that you’ve got an idea of the amount of money you need to accomplish your goal and how you’ll make it happen, you can figure out an estimated date when you’ll complete your goal. Woo!

If you’ve got an upcoming vacation or plan to pay cash for all Christmas gifts, those have pretty obvious completion dates. If you’re saving for a house or paying off debt, just give your best guess as to when you can reach your goal. It’s ok if you have to change your estimated completion date later on, just do your best.

It’s Monthly Budget Time!

Repeat after me: Budget is not a bad word. Budgets are good! Budgets make me happy!

A budget is simply a plan for your money. It’s deciding ahead of time how you will spend it instead of getting to the end of the month and wondering where all of your money went. It’s spending your money on purpose!

We plan our schedules on a calendar. We plan our vacations. We plan times to meet up with friends for coffee. All good things, right? And now we plan our money.

Before you worry that you’re going to have to buckle down and give up everything fun in life, let me be clear: your budget/plan for your money can be anything you want it to be!

If you can afford to eat out five nights a week and decide that that’s how you want to spend your money, that’s totally ok! We’re just going to decide it ahead of time with the monthly budget.

Remember those goals that you set? You probably aren’t making much progress toward them without a plan for how you’ll spend and save your money.

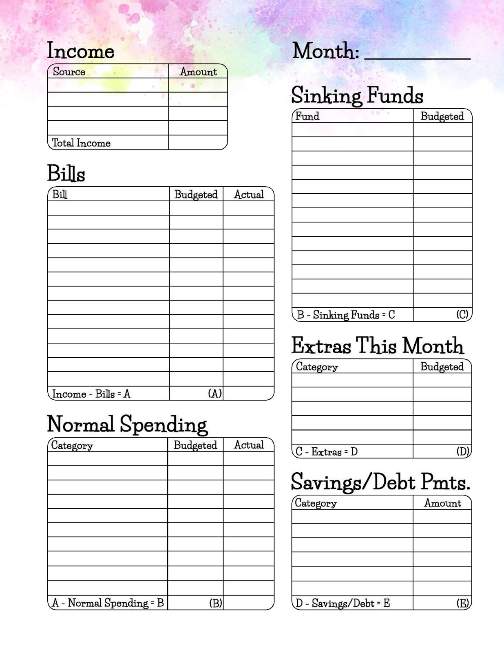

Your monthly budget will help you set priorities with your spending so that you can accomplish your goals and spend your money where you want to. The monthly budget printable will show you your plan for all of your money for the month.

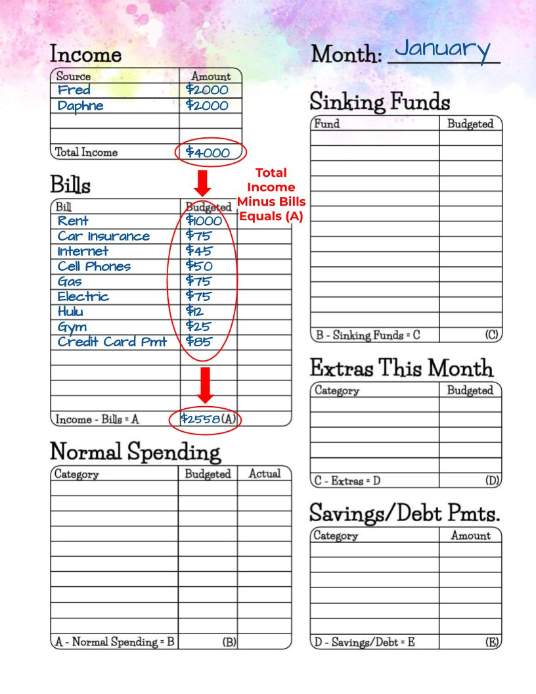

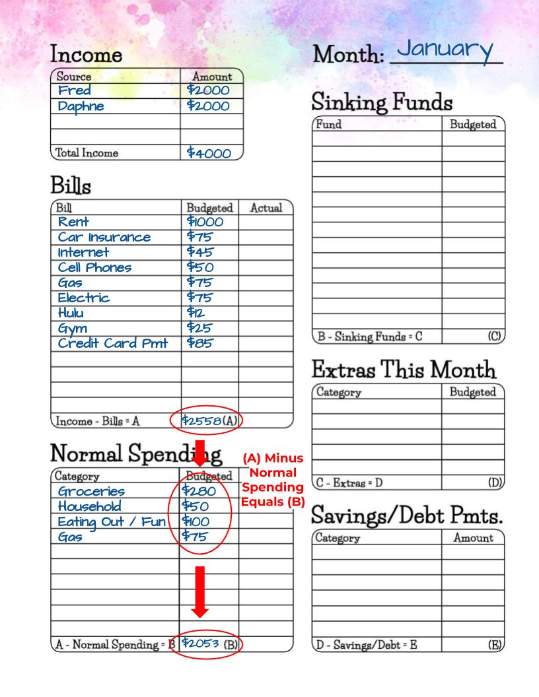

Start with the easy one: write down the month you’re budgeting for on the top right line.

Income

In the “Income” section, you’re going to write in all your income for the month. Write down where the money is coming from under “Source” and the amount under “Amount”.

Add in your spouse’s income if you have your finances combined.

If you have an irregular income, estimate on the lower end of what you usually bring in. If you make more, you can always figure out what to do with extra money later on.

Sidenote: Think about trying to get a month ahead with your income. At our house, we save all of the paychecks that come in to be used on the next month’s budget. So everything we make in November doesn’t get touched at all until December 1st. We know exactly how much money we have for December and have all of the money to pay our bills immediately, which simplifies things a lot. To make this happen, you’ll have to save up a full month’s worth of expenses, which might make a great goal to add to your goals list!

Ok, add up all of your income and write it down in the box next to “Total Income”. (DO NOT get hung up on the numbers in the examples below. They’re completely made up to show you how to use the printables. This system can work with any income.)

Bills

Next up, we’re going to write down all of your regular bills, plus the amounts of each.

List each bill under “Bills” and the amount you want to budget for each under “Budgeted”.

Most of your bills are probably the same each month, but you may need to choose an amount to budget for your utilities or cell phone bill if those can vary a bit.

Add in your minimum debt payments as well. We’ll handle paying extra on your debts in a different section, but for now we just want all of the minimum necessary bills.

Once you’ve written down all of your bills, take your “Total Income” amount and subtract all of your bills to figure out how much money you have left over for everything else. We’ll call this new total (A) .

Normal Spending

Time to budget for all of your normal monthly spending.

Things like:

● Groceries

● Household Items

● Gas

● Eating Out

These are you variable spending categories that happen every month. If you don’t know how much to budget for each of these categories, you can look back at your credit card or debit card accounts for the last month to get an idea.

Remember: It will not be perfect. Especially not your first time. You’ll probably need to make adjustments throughout the month and you’ll learn how to budget more accurately for next month. It’s a process, so just work through the plan.

Now you’re going to take your (A) amount from the bottom of your Bills section and subtract all of your budgeted amounts from your Normal Spending section. This will give you (B) , which is the amount you have left over for everything else.